Investigating the role of psychological elements in advancing IT skills among accounting students: insights from Saudi Arabia

Introduction

Nowadays, improving information technology (IT) skills is regarded as critical for the accounting field, as advanced technology has become an increasingly important component in financial management and reporting. While many factors influence the development of IT skills, psychological factors considerably influence university students’ ability to learn and excel at these skills. It is critical for educators and organizations seeking to improve IT skill development in accounting students to understand and address these psychological factors. Psychological factors, which include various cognitive and emotional processes (Rugulies 2019), have a direct impact on students’ learning capacity and proficiency in IT skills. According to Keskin (2019), these factors can either help or hinder students’ progress in learning and applying accounting technology. Professional educators who recognize and understand these influences can develop targeted teaching strategies and create a supportive educational environment, allowing students to reach their full academic potential. Rosalina et al. (2020) discovered that the psychological factors influencing IT skill development in accounting students are numerous and complex, including cognitive processes, motivation, self-efficacy beliefs, learning styles, and attitudes toward technology. Each individual factor, as well as their collective influence, plays a critical role in shaping students’ capacity to assimilate, utilize, and adapt to various information technology tools and applications. An examination of cognitive elements, encompassing attention, memory, problem-solving abilities, and critical thinking, provides insight into students’ interactions with IT systems and their efficacy in professional contexts. Additionally, the level of motivation significantly affects their commitment, perseverance, and eagerness to acquire and enhance IT competencies (Olszewski‐Kubilius et al. 2019). The beliefs students hold about their self-efficacy, reflecting their confidence in their own capabilities (Alnoor et al. 2020), play a pivotal role in their engagement with technology and their resilience when encountering difficulties. The learning styles and preferences of accounting students also dictate their approach to developing IT skills. Recognizing prevalent learning techniques, such as visual and auditory methods, allows educators to customize instructional strategies and incorporate suitable learning materials, thus fostering greater student involvement and proficiency in IT skills. Research by Rebele and Pierre (2019) indicates that students’ attitudes towards technology, along with their perceptions of its relevance and practicality in the field of accounting, significantly influence their motivation, learning outcomes, and development of IT skills. A positive mindset and belief in the utility of technology can foster students’ enthusiasm, interest, and willingness to experiment with and use new IT tools and applications. By assessing these psychological factors, this study offers insights and recommendations for institutions and educators looking to help accounting students improve their IT skills. Recognizing and addressing these factors allows educators to empower students, improve their learning experiences, and provide them with critical IT skills required for success in the dynamic field of accounting. The rapid advancement of IT has transformed the accounting profession, requiring accounting students to acquire and master IT skills. Gerli et al. (2022) and Pettersen et al. (2022) conducted investigations into the effects of psychological factors on the acquisition of IT skills. This body of research, however, reveals a notable deficiency in studies specifically targeting accounting students in Saudi Arabia. Acknowledging these factors within this particular demographic is vital for devising efficacious educational tactics and fostering a conducive academic milieu, as underscored by Gerli et al. (2022). Nevertheless, the precise psychological factors that shape IT skill development among accounting undergraduates at Saudi universities remain underexplored, a point highlighted by Krumrei-Mancuso et al. (2013; 2020). Therefore, pinpointing these elements is crucial for enhancing teaching methods in accounting education and equipping students with vital IT competencies. This research aims to assess the influence of psychological factors on IT skill advancement in accounting students in Saudi Arabia. Employing a quantitative survey approach, the study gathers comprehensive data on the psychological determinants affecting IT skill evolution from a broad spectrum of accounting students across different academic echelons in Saudi universities. The results of this investigation augment the existing knowledge on IT skill formation in accounting education and offer insights pertinent to Saudi Arabia and other Arab nations. It yields pivotal revelations and strategic guidance for educators and academic institutions striving to refine IT skill cultivation methods for accounting students. By scrutinizing psychological factors unique to the Saudi context, this research aids in customizing educational practices, providing adequate support, and initiating programs that promote thorough acquisition as well as IT proficiency among accounting students in Saudi Arabia.

Literature review

A variety of physiological elements that may influence the development of IT skills among accounting students have been identified in the literature review. These factors significantly affect an accountant’s proficiency in acquiring, applying, and comprehending IT.

Theories impacting psychological factors on IT skill development

Social Cognitive Theory (SCT) developed by Luszczynska, Schwarzer (2015), emphasizes self-regulation, self-efficacy, and observational learning in skill acquisition. Burke and Mancuso (2012) elucidate that individuals develop IT competencies through observing others, building confidence via successful endeavors, and orchestrating their learning journey. While SCT provides valuable insights into individual learning processes, it may underestimate the impact of rapidly evolving technological environments in accounting. As noted by Torre and Durning (2015) and Schunk and DiBenedetto (2020), SCT’s focus on individual cognitive aspects may not fully account for the collaborative nature of modern accounting practices and institutional influences. In the context of our study, SCT directly informs hypotheses H1 (cognitive abilities) and H2 (motor skills). The theory suggests that accounting students’ cognitive abilities and motor skills, shaped by their observations and social interactions, play crucial roles in their capacity to acquire and apply IT skills. For instance, students with higher self-efficacy in IT tasks may be more likely to persist in learning complex accounting software.

Csikszentmihalyi’s (1975) flow theory characterizes an optimal psychological state during engaging activities. Obadă (2019) notes that individuals are more likely to improve their IT skills when there’s a balance between their abilities and task demands. Flow theory offers insights into creating engaging learning experiences but may not fully address the need for systematic skill development in structured accounting curricula. As Clifford (1984) and Bonnes and Lee (2017) point out, the theory tends to ignore external factors like environmental conditions and social context. Flow Theory underpins our hypothesis H5 (fatigue and stress). It suggests that optimal learning and skill development occur when students are neither overwhelmed (leading to stress) nor under-challenged (potentially leading to fatigue or boredom). In the context of IT skill development in accounting, this theory supports our expectation that lower levels of fatigue and stress would positively influence skill acquisition, as students are more likely to achieve a state of flow.

Cognitive Load Theory (CLT) presented by Van Merrinboer and Sweller (2010), posits that the capability to acquire IT skills is contingent upon the cognitive effort demanded in the learning process. It suggests that effectively managing cognitive load facilitates IT skill development by refining instructional design and diminishing superfluous cognitive burden (Paas et al. 2003; Sweller 2020). CLT provides valuable guidelines for designing accounting IT curricula. However, its application must consider the diverse prior experiences and varying cognitive abilities of accounting students, which can significantly impact learning outcomes. CLT informs our hypotheses H3 (visual processing) and H4 (ergonomics). The theory supports our expectations that effective visual processing and ergonomic considerations would reduce extraneous cognitive load, thereby facilitating IT skill development. For example, well-designed accounting software interfaces that align with CLT principles could enhance students’ ability to learn and use these tools effectively.

Application to Current Research: Based on these theories, we hypothesize that IT skill development in accounting students is influenced by:

-

1.

Self-efficacy and observational learning opportunities (SCT).

-

2.

Balanced challenges in IT tasks (Flow Theory).

-

3.

Optimized cognitive load in learning materials and activities (CLT).

These theories collectively form a comprehensive framework for understanding the psychological factors influencing IT skill development in accounting students. By integrating SCT, Flow Theory, and CLT, we account for social learning processes, optimal engagement conditions, and cognitive resource management in skill acquisition.

Recent advances in IT skills development in accounting education

Recent studies have highlighted the growing importance of IT skills in accounting education globally. For instance, Handoko et al. (2024) emphasized the need for auditors to develop skills in emerging technologies like machine learning, which requires a combination of cognitive and motor skills for effective use of software tools. This aligns with our hypotheses H1 and H2, underlining the importance of both cognitive abilities and motor skills in IT skill development.

Nishikawa et al. (2024) explored the soft skills needed by accounting graduates in New Zealand, including digital competencies. Their findings highlight the need for accounting education providers to ensure graduates develop these sought-after skills alongside technical and IT competencies, supporting our holistic approach to examining psychological factors in IT skill development.

In the European context, Draganac et al. (2022) examined digital competencies among university and high-school students in selected European countries, finding that programming skills are lagging behind other digital competencies. This highlights the need for enhanced visual processing skills (H3) in interpreting and working with complex digital interfaces.

Gușe and Mangiuc (2022) analyzed the impact of digital technologies in Romanian accounting practice and education, illustrating universities’ potential for training specialists to assimilate and steer the digital transformation of the accounting profession. Their work underscores the importance of considering ergonomic factors (H4) in the increasingly digital accounting profession.

Hypotheses development

Cognitive abilities

Recent studies highlight the crucial role of cognitive abilities in IT skill acquisition for accounting students. Tsiligiris and Bowyer (2021) emphasize the need for accounting education to foster critical thinking and problem-solving skills in the context of digital technologies. Bahador and Haider (2020) identified four key approaches to enhancing IT skills among accounting practitioners: formal education, training, work experience, and job enrichment. This underscores the importance of cognitive abilities in various learning contexts.

These findings build upon earlier work by Furnham et al. (2003) and Demetriou et al. (2019), who established the significance of cognitive functions in skill development. Recent research by Peng and Kievit (2020) and Albulescu et al. (2023) further reinforces the connection between cognitive abilities and academic achievement in university environments. Therefore, this study proposes the following hypothesis:

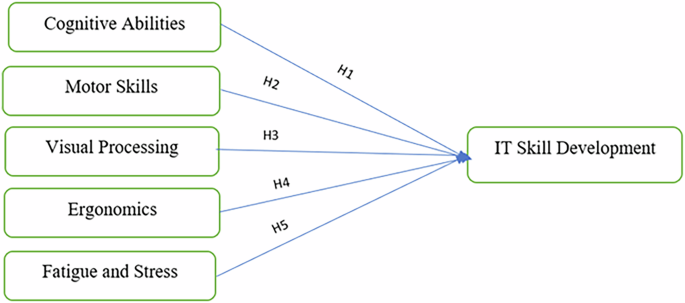

H1: A significant correlation exists between the development of IT skills and cognitive ability among accounting students in Saudi Arabia.

Motor skills

While traditionally associated with physical activities, motor skills have emerging relevance in IT skill development for accounting students. Recent studies by Handoko et al. (2024) highlight the importance of preparing auditors for emerging technologies like machine learning, which requires a combination of cognitive and motor skills for effective use of software tools. Taib et al. (2023) assess digital competencies among postgraduate accounting students, revealing moderate to high levels of digital competence. Gușe and Mangiuc (2022) analyze the impact of digital technologies in accounting and illustrate universities’ potential for training specialists to assimilate and steer the digital transformation of the accounting profession.

This builds on earlier work by Liu et al. (2020) and Aadland et al. (2017), who demonstrated a favorable association between motor skills and academic achievement among university students. The application of motor skills in accounting IT contexts may involve proficiency in using various software interfaces and data input methods. Therefore, the study posits the following hypotheses:

H2: A significant correlation exists between the development of IT skills and motor skills among accounting students in Saudi Arabia.

Visual processing

Visual processing plays a crucial role in IT skill development for accounting students. Recent work by Cevallos et al. (2023) on the use of accounting and auditing technological tools by university students underscores the importance of visual processing in interpreting complex financial data and using accounting software. Draganac et al. (2022) examine digital competencies among university and high-school students in selected European countries, finding that programming skills are lagging behind other digital competencies. This highlights the need for enhanced visual processing skills in interpreting and working with complex digital interfaces.

This aligns with earlier research by Wolff et al. (2021) and Lupyan et al. (2020) on the importance of visual processing in information interpretation. Sweller (2020) and Simanjuntak and Barus (2020) highlight the effectiveness of visual information in learning, particularly relevant in the context of accounting software and data visualization tools. Consequently, the study proposes the following hypothesis:

H3: A significant correlation exists between the development of IT skills and visual processing among accounting students in Saudi Arabia.

Ergonomics

The importance of ergonomics in IT skill development has gained increased attention, especially with the shift to remote learning and work. Grosu et al. (2023) investigate accountants’ perceptions of digitalization, highlighting the need for ergonomic considerations in the increasingly digital accounting profession.

This builds on earlier work by Boatca and Cirjaliu (2015) and more recent studies by Emerson et al. (2021) on the importance of ergonomic design in digital workspaces. Proper ergonomics can enhance learning efficiency and reduce physical strain associated with prolonged computer use. This leads to the subsequent hypothesis:

H4: A significant correlation exists between the development of IT skills and ergonomics among accounting students enrolled at colleges in Saudi Arabia.

Fatigue and stress

The impact of fatigue and stress on IT skill development is particularly relevant in the current educational landscape. Palanimally et al. (2024) investigate the distribution of skills and motivation to enhance resilience among accounting personnel during COVID-19, highlighting the importance of managing stress in skill development. Nishikawa et al. (2024) explore the soft skills needed by accounting graduates in New Zealand, emphasizing the importance of resilience and adaptability in the modern accounting profession. Their findings highlight the need for accounting education providers to ensure graduates develop these sought-after skills alongside technical and IT competencies.

This complements earlier work by Deckard et al. (2022) and Hatunoglu (2020) on the effects of stress on university students’ performance. Lee and Perdana (2023) further demonstrate how experiential learning approaches can help mitigate stress while improving data analytics competency among accounting students. This leads to the hypothesis that:

H5: A significant correlation exists between the development of IT skills and fatigue and stress among accounting students enrolled at colleges in Saudi Arabia.

In conclusion, there is a substantial interplay between these psychological factors and the development of IT abilities in accounting students. By integrating SCT, Flow Theory, and CLT, we account for social learning processes, optimal engagement conditions, and cognitive resource management in skill acquisition. Understanding and addressing these factors is crucial for the effective acquisition, use, and mastery of information technology in accounting education.

Research method

Our study employed a quantitative approach to investigate the psychological factors influencing IT skill development among accounting students in Saudi Arabia. We developed a comprehensive survey instrument that built upon and extended previous research in IT skills and ergonomics (Torkzadeh and Van Dyke 2002; Shikdar and Al-Kindi 2007; Tarafdar et al. 2007).

Survey development

The questionnaire’s development involved a rigorous process to ensure validity and reliability. We began by conducting an extensive literature review, drawing from established instruments such as the Computer Self-Efficacy Scale (Compeau and Higgins, 1995), the Technology Acceptance Model questionnaire (Davis 1989), the NASA Task Load Index (Hart and Staveland, 1988), and the Visual Processing Skills Questionnaire (Colarusso and Hammill, 1972).

We identified six key dimensions that influence IT skill development: Cognitive Abilities, Motor Skills, Visual Processing, Ergonomics, Fatigue and Stress, and IT skills. This multifaceted approach, inspired by the work of Karwowski et al. (2003) and Boulianne (2016), allowed us to capture a holistic view of the factors affecting students’ IT skill acquisition and use.

To ensure content validity, we consulted a panel of experts, including three accounting professors with expertise in IT integration, two IT professionals specializing in educational technology, and a psychologist specializing in educational psychology. Their feedback helped us tailor the questionnaire to the Saudi Arabian context and ensure its relevance to accounting education.

Pilot study and refinement

We conducted a pilot study with 35 participants, including 20 accounting students from various academic years, 10 recent graduates, and 5 accounting professionals. Based on their feedback, we refined the instrument, initially reducing the number of items from 70 to 52, simplifying language, and improving the logical flow of questions.

Following the pilot study, we analyzed the internal consistency of the items using factor loadings, Cronbach’s alpha, composite reliability, and average variance extracted. Items that did not meet the threshold for internal consistency were dropped. Specifically, we removed items CA4 and CA5 from Cognitive Abilities, EG1 from Ergonomics, FS4 from Fatigue and Stress, and MS1 and MS2 from Motor Skills.

The final questionnaire consisted of 46 items across the six dimensions, using a 5-point Likert scale, plus four demographic questions.

Sample and data collection

Our study population comprised accounting students from various Saudi Arabian universities. Using a combination of convenience and snowball sampling techniques, we distributed the questionnaire to students across different academic levels. This approach aligns with similar studies in educational research that have utilized convenience sampling to access student populations.

We collected data from 306 accounting students, which exceeded the minimum sample size of 138 as determined by G*Power 3.1 analysis (Faul et al. 2009). The analysis parameters included an effect size f² of 0.15 (medium effect), α error probability of 0.05, power (1-β error probability) of 0.95, and 5 predictors. Our sample size also aligns with the recommended range of 100–200 cases for PLS-SEM analyses to detect even small effect sizes (Hair et al. 2017; Kock and Hadaya 2018).

The distribution of respondents across universities was as follows: University of Hail (33%), North Border University (27%), King Faisal University (24%), King Saud University (9%), and Alqasim University (7%). This distribution represents a mix of institutions from different regions of Saudi Arabia, enhancing the generalizability of our findings.

However, we acknowledge that our sampling method may introduce potential biases. These could include variations in IT infrastructure and resources across different universities, potential differences in curriculum emphasis on IT skills in different institutions, and socio-economic factors that may vary by region and influence students’ exposure to technology. While our large sample size and diverse institutional representation help mitigate some of these concerns, the potential for regional biases should be considered when interpreting our results.

Future research could benefit from a more stratified sampling approach to ensure equal representation across different universities and regions in Saudi Arabia. This would allow for a more nuanced understanding of how geographical and institutional factors might influence IT skill development among accounting students in the country.

Data analysis

For data analysis, we utilized partial least squares-structural equation modeling (PLS-SEM), a method well-suited for handling multiple variables and exploring complex relationships (Sarstedt et al. 2020; Do Valle and Assaker 2016). This technique allowed us to examine the connections between our independent variables (the six psychological dimensions) and the dependent variable (IT skill development).

Ethical considerations

Throughout the study, we adhered to strict ethical guidelines. We obtained informed consent from all participants and ensured their anonymity and data confidentiality. The study received approval from the relevant institutional review board before commencing data collection.

While our study provides valuable insights, we acknowledge certain limitations. The cross-sectional nature of our data limits causal inferences. Future research could benefit from longitudinal designs to track IT skill development over time, as suggested by Ayyagari et al. (2011). Additionally, expanding the study to other geographic regions could enhance the generalizability of our findings.

Our methodology combines established research techniques with a novel, comprehensive framework for examining IT skill development among accounting students. By addressing multiple psychological dimensions, we aim to provide a nuanced understanding of the factors influencing students’ ability to acquire and utilize IT skills in their academic and future professional endeavors.

Data analysis and results

Demographics of the sample used

Most of the survey participants, comprising 226 individuals or 73.9%, were female. The academic levels of the respondents spanned from first to fourth year, with respective proportions of 19.6%, 32%, 27.5%, and 20.9%. Predominantly, the participants fell within the 21 to 25 age range, accounting for 85.6% of the sample. Table 1 presents the collated demographic data.

Measurement model results

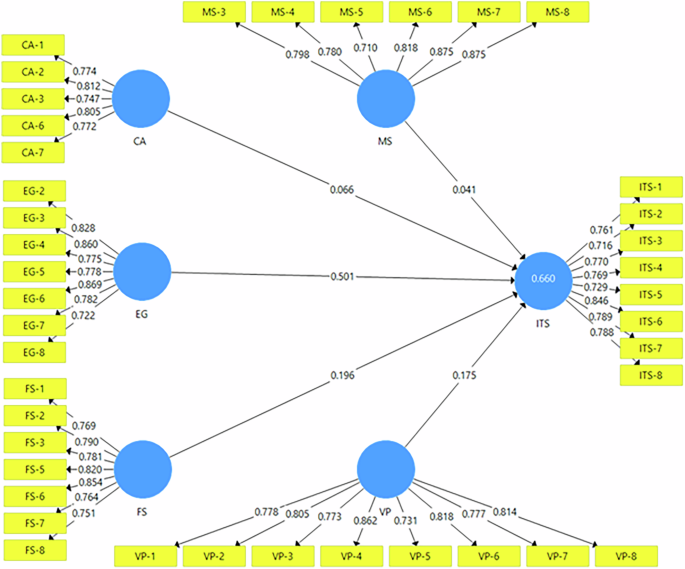

This study utilized PLS-SEM using SmartPLS 4 to assess the validity and dependability of the measurement model. By using SmartPLS 4, a thorough examination of the complete measuring framework was enabled. Kamis et al. (2020) state that this approach simultaneously evaluates measurement and structural models, allowing for the assessment of both convergent and discriminant validity of variables using factor analysis, as well as the testing of hypotheses. A comprehensive evaluation of the measurement model’s convergent and discriminant validity was conducted in this study. The study examined Cronbach’s alpha, composite reliabilities, average variance extracted (AVE), and factor loadings, all of which provided support for the claim of convergent validity. The findings of the study’s variables, including means, standard deviations, and factor loadings, are summarized in Table 2. Each unit of measurement contributed substantially to the latent construct to which it was matching. The range of factor loadings exceeded the 0.6 criterion that Ehido et al. (2020) suggested, spanning from 0.7156 to 0.8688. Using Cronbach’s alpha, the internal reliability of the measurement model was evaluated. In line with Vaske et al. (2017), and Bernardi (1994), a Cronbach’s alpha exceeding 0.7 is indicative of considerable content reliability. The alpha coefficients for all constructs in this study surpassed this threshold, with the lowest being 0.8418, indicating a high level of content reliability. Additionally, convergent validity was substantiated through an analysis of AVE and composite reliability, adhering to the minimum value of 0.6 as recommended by Valentini and Damasio (2016). The study’s composite reliability scores exhibited strong convergent validity, as they varied from 0.8473 for cognitive abilities to 0.9192 for visual processing.

To confirm a model’s convergent validity, Valentini and Damasio (2016) recommended that AVE values should exceed 0.5. As depicted in Table 2, all AVE values in this study exceeded this benchmark, further reinforcing the convergent validity of the test. Moreover, Valentini and Damasio (2016) proposed that in order to establish discriminant validity amongst constructs, the square root of AVE for a particular construct should exceed its correlation with other constructs. As indicated in Table 3, the correlation values in this investigation did not surpass 0.85, which allays worries over multicollinearity.

Results of hypotheses testing

The study employed the PLS-SEM bootstrapping method using SmartPLS 4 to test hypotheses. The findings, including parameter estimations, significance levels, and outcomes of hypothesis tests, are summarized in Table 4. The use of this technique enabled an examination of the factors that impact the development of information technology competencies among accounting students enrolled in colleges in Saudi Arabia.

There exists a considerable association between the growth of IT skills and cognitive capacities among accounting students enrolled in colleges in Saudi Arabia, according to Hypothesis 1. The statistics, however, indicated an other possibility. In regard to IT skill development, the standardized coefficient for cognitive abilities was 0.0664, accompanied by a t-value of 1.4854 and a p value of 0.1375, which indicate a lack of statistical significance. As a result, Hypothesis 1 is not supported by the data.

In contrast, Hypothesis 2 proposed a significant association between the development of IT abilities and motor skills within this particular cohort. In this particular scenario, the standardized coefficient for motor skills was found to be much greater at 0.5014. This conclusion was supported by a significant t-value of 9.1890 and a conclusive p value of 0.0000, which unequivocally demonstrate statistical significance. Hypothesis 2 is thus highly supported.

Similarly, Hypothesis 3 posited that certain students will gain IT skills in a manner that is both important and favorable in relation to their visual processing ability. The association in question exhibited statistical significance, as shown by the standardized coefficient of 0.1959, t-value of 4.3860, and p value of 0.0000. Therefore, Hypothesis 3 is unequivocally validated.

In Saudi colleges, accounting students were projected to have a significant correlation between ergonomics and IT skill development, according to Hypothesis 4. However, the statistics indicated an other conclusion. In relation to this, the standardized coefficient for ergonomics was 0.0415, which, when combined with a p value of 0.5333 and a t-value of 0.6230, indicated an absence of statistical significance. Consequently, Hypothesis 4 lacks empirical validation.

Finally, Hypothesis 5 posited that within the same population, there exists a positive correlation between stress, IT skill growth, and weariness. Indicating statistical significance, the standardized coefficient for tiredness and stress in connection to IT skill development was 0.1755, supported by a t-value of 2.3728 and a p value of 0.0177. These results conclusively demonstrate that there is a substantial correlation between stress, IT skill development, and weariness among accounting students attending colleges in Saudi Arabia; hence, Hypothesis 5 is completely supported.

Discussion

This research aims to scrutinize the psychological determinants impacting the acquisition of information technology competencies among accounting students in Saudi Arabian higher education institutions. The empirical evidence presented in this study substantiates the necessity of this exhaustive exploration.

Our findings both confirm and challenge existing literature, addressing several important research gaps. Previous studies such as Tsiligiris and Bowyer (2021) and Handoko et al. (2024) have primarily focused on general IT skill development or digital competencies, while our research specifically examines psychological factors within accounting education in Saudi Arabia. This addresses a significant gap in understanding how cultural and educational contexts influence IT skill development in specialized fields. Moreover, our findings regarding stress and fatigue align with recent work by Palanimally et al. (2024) and Nishikawa et al. (2024), who emphasized the importance of resilience in accounting education. However, our results on the non-significance of cognitive abilities and ergonomics challenge traditional assumptions in educational psychology research, suggesting that the relationship between these factors and IT skill development may be more context-dependent than previously thought. This unexpected finding extends the work of Boatca and Cirjaliu (2015) and Grosu et al. (2023), indicating that established theories about cognitive abilities and ergonomics may need refinement when applied to specific educational contexts Fig. 1.

Conceptual framework.

Our Partial Least Squares (PLS) analysis, as illustrated in Fig. 2, elucidate pivotal factors that either facilitate or hinder IT proficiency in these academic settings. Notably, fatigue and stress emerged as predominant factors, explaining 19% of the variance in IT competency among the student cohort. This finding aligns with recent research by Palanimally et al. (2024) and Nishikawa et al. (2024), which emphasize the importance of resilience and stress management in accounting education and practice. It also corroborates earlier work by Deckard et al. (2022), Akter (2021), and Hatunoglu (2020), supporting the notion that these components are significant in the development of IT competencies. The substantial impact of stress and fatigue on IT skill development underscores the need for a holistic approach to accounting education that considers students’ psychological well-being alongside their technical skills.

Analytical results.

Visual processing emerged as a more substantial factor, explaining 17% of the variance in IT skill development. This finding supports the work of Cevallos et al. (2023) and Draganac et al. (2022), as well as earlier studies by Sweller (2020), Simanjuntak and Barus (2020), Goldstand et al. (2005), and Hopkins et al. (2019), all of which highlight the importance of visual competencies in interpreting complex data and using software tools.

Our study found that motor abilities have a relatively small but significant impact on IT skill development, accounting for 4% of the variance. While this effect seems modest, it is consistent with previous research highlighting the importance of motor skills in academic achievement and professional development (Aadland et al. 2017; Macdonald et al. 2020; Davis-Pollard et al. 2023. The work of Handoko et al. (2024) further underscores the relevance of motor skills in the context of emerging technologies like machine learning in auditing. This finding suggests that even in a field traditionally seen as cognitive, physical skills play a role in technological proficiency.

Contrary to our initial hypotheses and some previous research (Furnham et al. 2003; Demetriou et al. 2019), our study indicates that cognitive abilities and ergonomics do not significantly impact IT skill development in this context. This unexpected finding aligns with Boatca and Cirjaliu’s (2015) work, suggesting that the relationship between cognitive abilities, ergonomics, and IT skill development may be more complex or context-dependent than previously thought.

Several potential explanations for these unexpected results warrant consideration. The unique cultural and educational landscape of Saudi Arabian universities may play a crucial role in shaping how cognitive abilities and ergonomics influence IT skill development. For instance, educational systems that emphasize rote learning, as highlighted by Alkhateeb (2013) in Saudi education, might inadvertently diminish the impact of general cognitive abilities on IT skill acquisition.

Moreover, the measures we employed for cognitive abilities and ergonomics may not have fully captured the nuanced aspects most pertinent to IT skill development in accounting. This measurement limitation suggests that future studies could benefit from more specialized, domain-specific measures to better understand these relationships, aligning with Ballantine et al. (2008) emphasis on the need for context-specific cognitive measures in accounting education research.

Another possibility is the presence of compensatory effects. Other factors, such as individual motivation or specific training practices implemented in these universities, might offset variations in cognitive abilities or ergonomic conditions. This compensation could lead to the apparent lack of significant impact we observed in our study. Tan and Laswad’s (2015) discussion of how motivational factors could compensate for other variables in accounting education supports this explanation.

Lastly, we must consider the potential existence of threshold effects. There might be a certain level of cognitive ability or ergonomic condition beyond which further improvements do not significantly impact IT skill development. If the majority of students in our sample were already above this threshold, it could explain why we didn’t observe a significant effect. This concept of threshold effects in skill development is supported by research in other fields, such as Ackerman’s (2007) work on cognitive abilities and skill acquisition.

The R² value of 0.6596 for our model indicates that the identified psychological factors explain a substantial portion (approximately 66%) of the variance in IT skill development. This robust explanatory power underscores the importance of considering these psychological factors in accounting education and IT skill development programs.

Our findings carry significant practical implications for educators and policymakers in the field of accounting education, particularly within the Saudi Arabian context. The study reveals a complex interplay of psychological factors influencing IT skill development, each demanding careful consideration in curriculum design and educational policy.

Foremost among these factors is the impact of fatigue and stress on IT skill acquisition, accounting for a substantial 19% of the variance in our model. This finding underscores the critical need for educational institutions to prioritize stress management techniques within their accounting curricula. Imagine a learning environment where mindfulness or relaxation sessions are seamlessly integrated into IT-related courses, providing students with valuable tools to manage the cognitive demands of technology adoption. Time management workshops, tailored specifically to the unique challenges of IT skill acquisition in accounting, could equip students with strategies to balance their workload effectively. Moreover, the provision of specialized counseling services for students grappling with technology-related stress could offer a crucial support system, fostering resilience and adaptability. These recommendations align closely with recent research by Palanimally et al. (2024), who emphasized the importance of enhancing resilience among accounting personnel in an increasingly digital professional landscape.

Visual processing emerged as another key factor, explaining 17% of the variance in IT skill development. This insight calls for a shift towards more visually-oriented teaching methods in accounting education. Educators might consider increasing the use of data visualization tools in accounting software training, helping students to interpret complex financial information more intuitively. The incorporation of graphical representations of intricate accounting concepts could enhance comprehension and retention. Additionally, developing visual-based tutorials for new IT tools could accelerate the learning process, making technology adoption less daunting for students. This approach finds support in the work of Cevallos et al. (2023), who highlighted the crucial role of visual competencies in interpreting complex financial data in today’s digital accounting environment.

While motor abilities had a comparatively smaller impact, explaining 4% of the variance, their significance should not be overlooked. This finding suggests a need for more hands-on, practical exercises in IT skill development for accounting students. Educators could design interactive, hands-on training sessions with accounting software, allowing students to develop muscle memory and familiarity with essential tools. The incorporation of gamification elements requiring physical interaction with IT tools could make learning more engaging and effective. Even seemingly simple interventions, such as developing typing and mouse accuracy exercises specific to accounting tasks, could yield significant improvements in overall IT proficiency. These recommendations build upon the findings of Handoko et al. (2024), who underscored the relevance of motor skills in the context of emerging technologies like machine learning in auditing.

Perhaps most intriguingly, our study found that cognitive abilities and ergonomics did not significantly impact IT skill development, a finding that challenges existing assumptions in accounting education. This unexpected result suggests that educators might need to shift their focus from enhancing general cognitive abilities to developing more specific, IT-related skills. While ergonomic considerations shouldn’t be entirely disregarded, our findings indicate that resources might be more effectively allocated to other areas of IT skill development. This discovery stands in contrast to earlier work by Furnham et al. (2003) and Demetriou et al. (2019), highlighting the need for context-specific research in accounting education, particularly as it relates to technology adoption and skill development.

In essence, our findings paint a nuanced picture of IT skill development in accounting education, one that calls for a multifaceted approach addressing stress management, visual learning, practical skill development, and a reconsideration of traditional assumptions about cognitive abilities and ergonomics. By implementing these insights, educators and policymakers can create more effective, student-centered learning environments that better prepare future accountants for the technological demands of their profession.

Our study extends previous research by integrating multiple psychological factors and quantifying their interrelationships, providing a more comprehensive understanding of IT skill development in accounting education. This holistic approach addresses Tsiligiris and Bowyer’s (2021) call for a more nuanced understanding of skill development in the context of the Fourth Industrial Revolution.

Moreover, our findings both confirm and challenge existing literature. For instance, the significant impact of stress and fatigue aligns with recent work by Nishikawa et al. (2024) on the importance of soft skills, including resilience, in accounting education. However, our results on cognitive abilities contrast with traditional views in educational psychology, such as those presented by Peng and Kievit (2020), suggesting that the relationship between cognitive abilities and skill development may be more complex in the specific context of IT skills in accounting.

The lack of significant impact from ergonomics is particularly intriguing when compared to studies like Grosu et al. (2023), which emphasized the importance of ergonomic considerations in the digital accounting profession. This discrepancy highlights the need for more nuanced, context-specific research in accounting education, particularly in rapidly evolving technological environments.

The unexpected non-significance of cognitive abilities and ergonomics warrants deeper examination within our study context. These findings suggest that the relationship between these factors and IT skill development may be more complex than initially theorized. Cognitive abilities might interact with other variables in ways our model didn’t capture—for instance, the structured nature of accounting education could mediate their impact on IT skill development. Similarly, ergonomic factors might interact with institutional infrastructure and available resources in ways that weren’t directly measured. The cultural and educational context of Saudi Arabian universities may also play a role in these relationships. For example, standardized teaching approaches might reduce the variation in how cognitive abilities influence skill development, while institutional similarities in computer facilities could minimize the impact of ergonomic factors. These potential interactions highlight the need for more nuanced measurement approaches in future studies examining these relationships.

Our findings on the importance of visual processing align well with broader trends in educational technology, as highlighted by Draganac et al. (2022) in their study of digital competencies. This suggests that accounting education may need to place greater emphasis on visual literacy and data visualization skills to prepare students for the increasingly visual nature of financial data analysis.

In conclusion, our study provides a nuanced picture of IT skill development in accounting education, highlighting the complex interplay of psychological factors. The significant roles of fatigue, stress, visual processing, and motor skills, coupled with the unexpectedly limited impact of cognitive abilities and ergonomics, both confirm some existing research and challenge other assumptions. These results provide a foundation for future research and practical applications in the rapidly evolving field of accounting education and IT skill development.

Conclusion

The advancement of IT capabilities among accounting students in selected Saudi Arabian universities is of paramount importance in today’s digital age. This study, utilizing PLS-SEM methodology, marks the initial empirical foray into the principal psychological factors affecting IT skill development within Saudi Arabian universities.

Our research identifies and empirically examines elements influencing IT skill development, highlighting the criticality of fatigue, stress, visual processing, and motor skills as key determinants impacting students’ engagement with digital technology. Through the testing of five hypotheses, this investigation confirms the substantial influence of these factors on IT skill development in these educational settings. Notably, three hypotheses related to fatigue and stress, visual processing, and motor skills are supported by the data, while two hypotheses concerning cognitive abilities and ergonomics are refuted.

This research makes a substantial scholarly contribution by facilitating the formation of a conceptual framework about the influence of psychological elements on the development of IT competencies within the Saudi Arabian setting. It integrates these factors to elucidate their interactions and quantify their collective impact, explaining approximately 66% of the variance in IT skill development.

The outcomes carry substantial implications for policy and practice in Saudi Arabia and similar contexts:

-

1.

Stress Management in Curriculum Design: Educational institutions should consider integrating stress management techniques and resilience training into their accounting curricula.

-

2.

Emphasis on Visual Learning: Accounting educators should prioritize visual learning methods, including greater use of data visualization tools and graphical representations of accounting concepts.

-

3.

Motor Skills Development: Incorporation of more hands-on, practical exercises with accounting software and IT tools could enhance relevant motor skills.

-

4.

Rethinking Cognitive Abilities: A shift towards more practical, application-based learning rather than emphasizing theoretical cognitive skills may be beneficial.

-

5.

Ergonomics in IT Education: Establishing baseline ergonomic standards for educational institutions could ensure a minimum level of comfort and safety in IT learning environments.

-

6.

Personalized Learning Approaches: Exploring more personalized learning pathways that cater to individual students’ strengths and challenges could be valuable.

-

7.

Policy Implications: Policymakers might prioritize funding for stress management programs or visual learning tools in accounting education.

Despite its contributions, it is essential to recognize the limitations of this research. First, the cross-sectional nature of our data limits our ability to capture how IT skills develop dynamically over time, suggesting the need for longitudinal approaches in future research. Second, the study’s scope was confined to Saudi Arabia, potentially limiting generalizability to other cultural and educational contexts. Third, our measures of cognitive abilities and ergonomics, while based on established instruments, may benefit from further refinement to better align with IT learning contexts in accounting education. Additionally, demographic factors were not thoroughly examined as potential mediating or moderating variables.

To address these limitations and further advance our understanding of IT skill development in accounting education, we propose several directions for future research. Comprehensive factor analysis should incorporate a broader range of variables, including technological, pedagogical, and environmental factors, to provide a more holistic understanding of IT skill development. Future research should extend beyond Saudi Arabia to validate the model’s broader applicability. This expansion would enable valuable international comparisons across different educational and cultural contexts. Comparative studies across various Middle Eastern countries could reveal important regional patterns in how psychological factors influence IT skill development, while investigating these relationships in developed economies would test the model’s generalizability across different educational systems and cultural contexts. Such cross-cultural research would provide insights into whether the influence of psychological factors on IT skill development varies across different educational frameworks and cultural settings, ultimately contributing to a more comprehensive understanding of IT skill development in accounting education globally. Longitudinal research is essential to track the evolution of IT skills over time and establish stronger causal relationships between psychological factors and skill development outcomes. The implementation of mixed-methods approaches, combining quantitative methods with qualitative insights, would provide deeper understanding of how students develop IT competencies. Intervention studies should test the effectiveness of specific educational strategies based on our findings, potentially leading to improved teaching methodologies. Demographic analysis would be valuable to examine how various demographic factors moderate the relationships between psychological factors and IT skill development. Future studies should incorporate objective skill assessments alongside self-reported data to provide more reliable measures of IT competency. Finally, technology-specific studies should focus on skill development for emerging technologies in accounting, such as artificial intelligence, blockchain, and data analytics tools, to ensure research remains relevant to evolving industry needs.

In conclusion, this study contributes to a more comprehensive understanding of IT skill development among accounting students by highlighting the complex interplay of psychological factors involved. As the accounting profession continues to evolve in response to technological advancements, understanding and addressing these factors will be crucial in preparing students for successful careers, ensuring that future accountants are not only technically proficient but also psychologically equipped to leverage IT effectively in their professional roles.

Responses